Trend Analysis Report

7-Day & 30-Day Market Intelligence

As of March 5, 2026 | Sources: Canadian Black Book, AutoTrader, Clutch, DesRosiers Automotive, OPENLANE

Executive Summary

Canada’s used vehicle market is entering March 2026 in a state of measured softening, following brief seasonal gains in early January. Wholesale values have edged lower over the past 30 days as rising supply meets cautious buyer activity, while retail prices remain structurally elevated well above pre-pandemic levels. Key pressures — including tight inventory from pandemic-era production gaps, ongoing Canada-U.S. trade tariff uncertainty, and shifting segment demand — continue to shape the landscape.

| Key Takeaway — 7 DaysCanadian Black Book’s week-ending February 28 data confirms continued modest wholesale price declines across all segments, with car, truck, and SUV categories all softening. Auction sell rates are mixed, with selective buyers facing firm seller floor prices. |

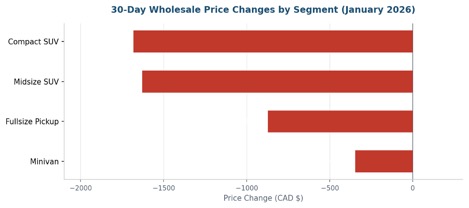

| Key Takeaway — 30 DaysJanuary 2026 saw broad negative price movement: Compact SUVs fell ~$1,682 (-7.4%), Midsize SUVs dropped ~$1,629 (-5.9%), Fullsize Pickups declined ~$873 (-2.4%), and Minivans slipped ~$347 (-1.5%). These declines partly reflect seasonal patterns and increased incentive activity. |

7-Day Trend Analysis (Week Ending Feb 28, 2026)

Weekly Wholesale Direction Scorecard

Canada’s used wholesale vehicle market continued to soften in the final week of February. Overall wholesale values declined modestly, continuing an adjustment trend driven by rising supply and cautious buyer behaviour.

Figure 1 — 7-Day Wholesale Market Direction by Segment (Week Ending Feb 28, 2026)

Segment Detail

| Segment | 7-Day Direction | Key Dynamics |

| Cars (all types) | ↓ Modest Decline | Continued normalization from pandemic highs |

| Trucks | ↓ Softening | Broader weakening across most configurations |

| SUVs / Crossovers | ↓ Softening | Post-tariff-rush demand cooling |

| Clean / Retail-Ready Units | → Stable / Firm | Persistent strong demand from retail channel |

Auction & Policy Notes

- Auction sell rates remain mixed: sellers hold firm floor prices while buyers stay selective, weighing on transaction velocity.

- Ford Motor Co. delayed planned three-row electric SUVs, shifting toward smaller EVs — affecting future used EV supply expectations.

- Honda Canada faces dealer backlash over proposed EV margin cuts of up to 44%, with Canadian Automobile Dealers Association intervening.

- Canada tightened auto import rules (March 3) to push local production, with implications for future model mix and MSRP levels.

30-Day Trend Analysis (February 2026)

Segment Price Changes

January 2026 wholesale data revealed broad-based declines across all major segments. The sharpest drops hit compact and midsize SUVs — the categories that had surged most dramatically during the 2024–2025 tariff-rush demand wave.

Figure 2 — 30-Day Segment Wholesale Price Changes, January 2026 (CAD $)

Retail Price Trend

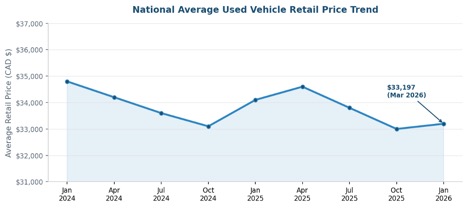

The national average used vehicle retail price stands at approximately $33,197 (Clutch, early 2026) — up 0.61% month-over-month but down 2.65% year-over-year. While this represents a meaningful decline from the 2022–2023 peak, prices remain dramatically elevated versus pre-pandemic norms, with Automotive News noting values are up more than 50% since 2020.

Figure 3 — National Average Used Vehicle Retail Price Trend (CAD $)

Segment Share

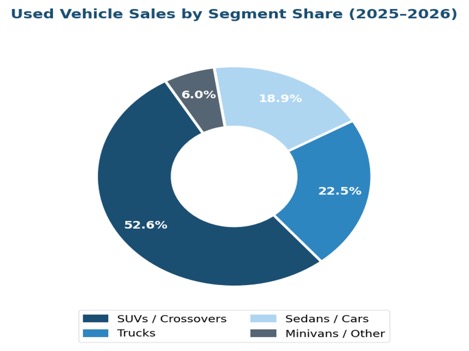

SUVs and crossovers continue to dominate the used market, holding approximately 52.6% of sales volume. Trucks remain a powerful secondary segment, particularly in Western Canada, while sedans have structurally declined.

Figure 4 — Used Vehicle Sales by Segment Share (2025–2026)

Supply & Inventory Conditions

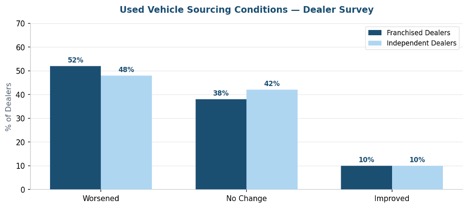

Inventory sourcing remains the dominant structural concern for Canadian dealers heading into 2026. A DesRosiers Automotive Consultants survey found that approximately 52% of franchised dealers and 48% of independents reported that sourcing conditions worsened over the past six months.

Figure 5 — Dealer Sourcing Conditions Survey: Franchised vs. Independent (%)

- Franchised dealers acquired 65.4% of used inventory directly from consumers; independents relied primarily on auctions (50.6% of supply).

- Pandemic-era production gaps (est. 1.5M fewer vehicles 2020–2023) continue to suppress lease return volumes and constrain off-lease supply.

- January 2026 auto sales were approximately 114,000 units — a ~3% YoY decline — reflecting cautious consumer sentiment and challenging weather.

- Canadian counter-tariffs on U.S. goods reduced used vehicle exports to the U.S., keeping more inventory in the domestic market.

Macro Factors & Trade Policy

Canada-U.S. trade dynamics remain the single largest wild card for the used vehicle market. U.S. 25% tariffs on Canadian goods disrupted supply chains and elevated new vehicle prices, driving substitution demand into used vehicles. This effect has begun to moderate as tariff-rush pull-forward demand from 2025 fades.

| Factor | Market Impact | Outlook |

| U.S. 25% tariffs on Canadian vehicles | Raised new-vehicle costs → pushed buyers to used | Ongoing; CUSMA review July 2026 |

| Canadian counter-tariffs | Slowed used exports to U.S. → more domestic supply | Partially positive for buyers |

| Pandemic production gap (2020–23) | 1.5M fewer lease returns; tight off-lease supply | Persisting through 2027+ |

| TD Economics 2026 forecast | Vehicle sales projected to fall ~4.3% in 2026 | Headwind for new; supports used |

| Auto import rule tightening | May shift model mix; potential MSRP ripple | Developing |

Near-Term Outlook

The market is entering the seasonally positive spring selling period — historically the strongest price recovery window of the year. After back-to-back seasonal declines in fall and early winter 2025, spring 2026 tailwinds are expected, but magnitude will depend on whether 2025’s tariff-rush surge repeats or normalizes.

| Indicator | Direction | Notes |

| Wholesale prices (7-day) | ↓ Softening | Modest declines continuing |

| Retail average price | → Stable / slight ↓ | Down YoY, up MoM |

| Spring seasonal demand | ↑ Historically positive | Strongest seasonal window of year |

| Inventory availability | → Gradually increasing | Still below pre-pandemic norms |

| EV used prices | ↓ Declining YoY | More supply, falling averages |

| Overall 2026 sales volume | ↓ Forecast -4.3% | Per TD Economics |

| Analyst NoteAutoTrader’s Q3 2025 Price Index observed that ‘much will depend on the availability of both new and used vehicles, ongoing trade policy developments, and broader economic conditions’ — a statement equally applicable entering Q1 2026. Buyers who benchmark against real market ranges rather than advertised markdowns are best positioned in this environment. |

Sources

- Canadian Black Book — Weekly Used Vehicle Wholesale Analysis (week ending Feb 28, 2026)

- Canadian Auto Dealer — ‘Used wholesale vehicle prices edge lower’ (March 4, 2026)

- Canadian Auto Dealer — ‘Used vehicle sourcing still tight, dealers say’ (Feb 2026)

- OPENLANE Canada — Canadian Vehicle Price Index (January 2026 update)

- AutoTrader Canada — Q3 2025 Price Index Report

- AutoTrader Canada — Q4 2025 Price Index Report

- Clutch — Rearview Recap 2025: Used Car Pricing Report

- TD Economics — ‘2026 Canadian Automotive Outlook’

- Automotive News — ‘Canadian used car prices to stay elevated’ (Feb 2026)

- Mordor Intelligence — Canada Used Car Market Report 2026–2031

- Car Dealership Guy News — ‘Canada tightens auto import rules’ (March 3, 2026)